Operational Alpha Newsletter: Mega-Funds Bought Their AI in April

Apr 28, 2026

|

Powered by G3NR8 OPERATIONAL ALPHA The PE Operating Partner Newsletter · Issue #6

|

April 28, 2026 · 9 min read · Tom Head

|

Key Takeaways ▶ Vista Equity x Google Cloud: agentic AI across 90+ software portcos. Largest PE-AI infrastructure deal of 2026 (22 April) ▶ KKR x Global Technical Realty: $1.5bn into European data centres + Oak Hill $400m. Total $1.9bn (7 January) ▶ Shield AI Series G: $1.5bn raise at $12.7bn valuation, $500m Blackstone preferred. Mega-funds now buying AI vendors, not just deploying them ▶ Enterprise AI in production: 72% in 2026, up from 55% in 2024 and 20% in 2020. Saturation, not adoption (a16z) ▶ OEX Marketing Intelligence deployment: 4.5 FTEs of manual work eliminated, under 12 weeks to production |

|

90+ Vista portfolio companies onto Google Cloud's agentic AI stack |

$1.9bn KKR + Oak Hill into Global Technical Realty (Jan 2026) |

72% of enterprises now run AI in production (a16z 2026) |

AI insights for PE funds, portcos and operating partners. No fluff, just useful cases, ROI, and keeping at the edge of where we’re headed.

Large Funds: AI Strategies

Vista signed the biggest PE-AI infrastructure deal of the year. KKR doubled down on the physical AI layer in Europe. And the mega-funds put $2bn behind a single AI defence company.

|

Vista Equity Partners x Google Cloud On 22 April, Vista signed a multiyear deal with Google Cloud to deploy agentic AI across its 90+ software portfolio companies. The package: Gemini, the AI Hypercomputer super-computing system, and Gemini Enterprise for building portco-specific AI agents. Largest single PE-AI infrastructure agreement since the Anthropic and OpenAI joint venture talks broke in March, and it is signed and in market, not in negotiation. Vista’s Agentic Factory now has Google’s stack plugged in directly. Source: Google Cloud / Bloomberg, 22 April 2026 |

|

KKR commits $1.5bn to Global Technical Realty On 7 January, KKR committed an additional $1.5bn to Global Technical Realty (GTR), a European data centre platform, with Oak Hill Capital adding $400m for nearly $2bn total. Same playbook as the $800m Singtel stake in Asia-Pacific. KKR is buying the physical layer that AI has to run on, in every region where its portfolio operates. Funds that own the picks-and-shovels will be quoting their portcos preferred power, preferred latency, and preferred pricing. Everyone else will be paying retail. Source: KKR / Oak Hill Capital, 7 January 2026 |

|

Shield AI: $1.5bn Series G at $12.7bn valuation On 26 March, Shield AI closed a $1.5bn Series G co-led by Advent International and JPMorgan Chase’s Security and Resiliency Initiative, plus $500m of Blackstone preferred equity and a $250m delayed-draw facility, at a $12.7bn valuation. Advent chairman David Mussafer joins the board. The structure echoes the OpenAI joint venture terms: PE preferred equity, board influence, defined enterprise commitments. Mega-funds are no longer just deploying AI to portcos, they are taking governance positions in the AI vendors themselves and routing the advantage back through the portfolio. Source: TechCrunch / Fortune, 26 March 2026 |

The pattern: mega-funds are buying the picks and shovels (data centres, model access, AI defence companies) and routing those advantages through their own portfolios. Mid-market funds cannot replicate that capex, but they can compete on AI speed-to-deployment.

Get in touch to discuss how.

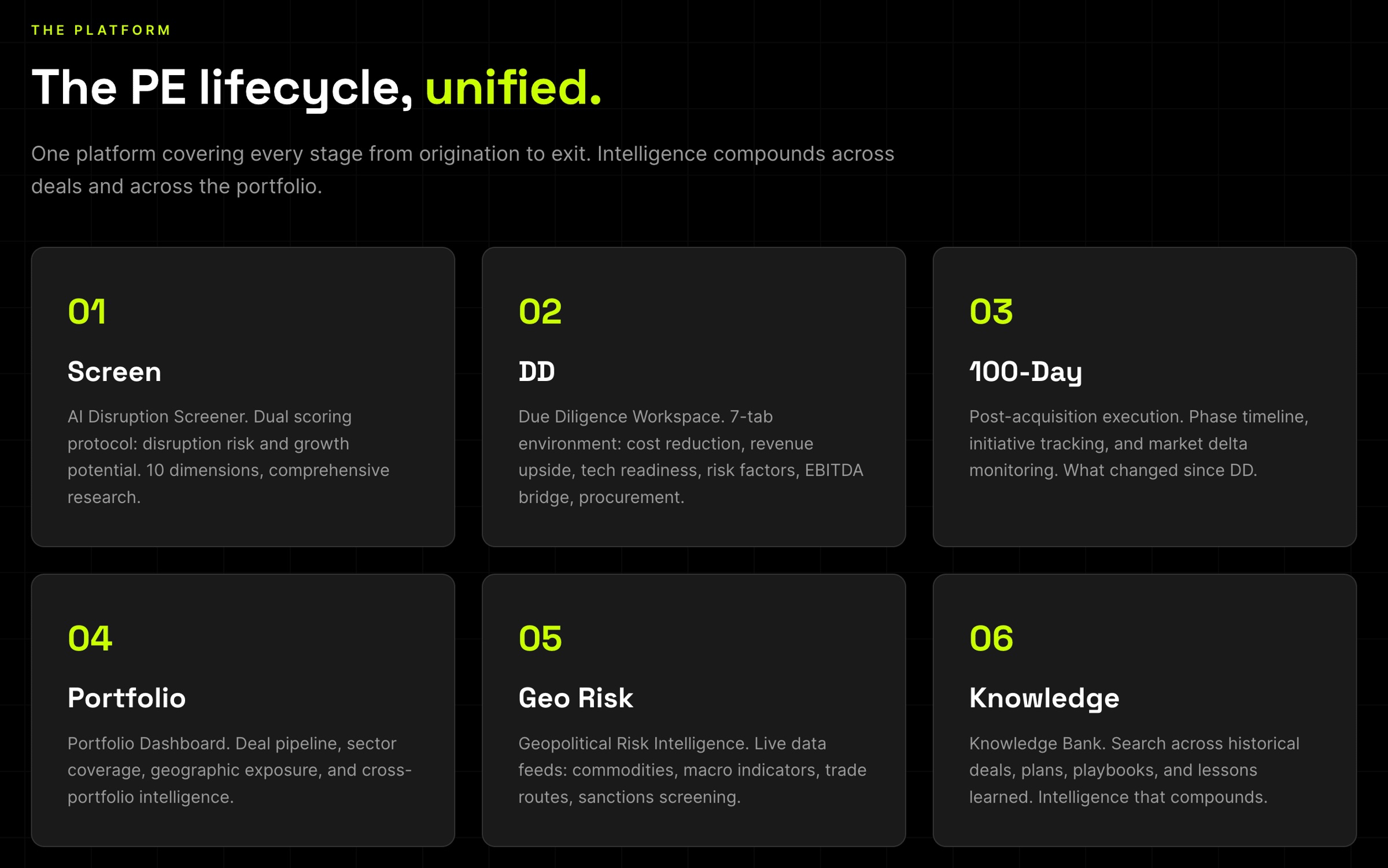

PE Intelligence: Origination to Exit

Our PE Intelligence Platform covers every stage from origination to exit. Screening, due diligence, 100-day execution, and portfolio monitoring. Intelligence that compounds across deals and across the portfolio.

|

PE Intelligence Contact us with ‘Intel’ in the subject and we’ll send you the latest insights we’ve found working with funds and portcos. |

Enterprise AI: Are Your Portcos Outliers?

72% of enterprises now run AI in production, up from 20% in 2020. That is not adoption any more, it is saturation. The portcos still treating AI as a roadmap item are now on the outside.

|

Chart 1 · Enterprises with AI in production % of enterprises, 2020 → 2026

Restyled from a16z Enterprise AI Pulse, April 2026. S-curve steepened through 2024 and is now at deployment saturation pace. |

Translate to PE: the software-led portcos you own are being compared to that experience every quarter by their own customers. A portco with no AI in production is not standing still, it is drifting backwards relative to the people buying from it.

What to do with this: in underwriting, treat AI in production as an exit-ready baseline, not a future capability. Chart the portco against that 72% line. Anything below is a gap, and gaps compress exit multiples.

The AI Edge: Systems and Early Warnings

Operating groups have doubled since 2021. AI is now in 73% of due diligence, up from 24%. Carve-outs are at a record 71% of PE activity. Top-decile funds are using all three shifts to pull ahead. Here is how.

|

1. They run portfolios as a system, not a set of LP commitments Operating groups have doubled since 2021 and 60% of firms now deploy ops teams during DD (McKinsey). Apollo’s cross-portfolio procurement AI across 40+ portcos is the canonical example. Source: McKinsey Global Private Markets 2026 |

|

2. They build their own operational early warning 91% of US leveraged loans are covenant-lite (LCD) and default rates hit 5.7% in early 2025, so the loan docs give lenders almost no warning. Top-decile firms run revenue-at-risk dashboards, order book intelligence, margin erosion signals and churn scoring across the portfolio. Source: LCD / PitchBook, Bain Global PE Report 2026 |

|

3. They treat carve-outs as AI-native deployment environments 71% of PE firms are pursuing carve-outs in 2026, 77% say activity is rising, and AI in DD is now at 73%, up from 24% (KPMG). Carve-outs arrive without legacy data infrastructure, ERP change-control politics or parent-company IT governance, which is the best deployment ground a top-decile fund could ask for. Source: KPMG Global M&A Outlook 2026 |

The payoff: the fund that closes its next raise will be the one that can show an LP three things: a portfolio run as a system, operational early warning across the portfolio, and a carve-out deployment playbook. Not slideware. Deployments. Talk to us about speed-to-EBITDA.

Real Use Case: Marketing Intelligence

A PE-backed global technology and engineering firm. The marketing team were already using AI at the desk level, but the experimentation was scattered and very little coordinated value was landing anywhere measurable.

We deployed our OEX platform with three pieces working as one: a centralised knowledge base, AI search with natural-language querying, and an automated repurposing engine that turns source content into channel-ready, multi-language outputs in minutes.

|

4.5 FTEs of manual work eliminated, under 12 weeks to production. Source: G3NR8 OEX deployment, PE-backed global tech and engineering firm |

What we delivered:

| ▶ 4.5 FTEs of manual work eliminated |

| ▶ Source content in, channel-ready outputs in minutes |

| ▶ Under 12 weeks to production |

| ▶ Scales across teams, languages and geographies |

We are now compounding value with the team: scheduled automation for case studies, Google Ads formats, expanded persona targeting, and smarter search across the knowledge base.

Why this matters for your portfolio: every portco has content, knowledge and IP trapped in people’s heads and buried in folders. The right platform eliminates headcount pressure, scales across teams, and gets smarter every week. Talk to us about creating operational efficiency with AI in weeks.

What I’m Reading

|

The PE AI Proof Gap - The gap between AI activity and AI proof is the defining problem in PE operations. (G3NR8) |

|

AI & the Labour Market - Measuring AI displacement risk by combining theoretical LLM capability with real-world usage data. (Anthropic Economic Index) |

|

AI Principles for Boards - “AI brings boards into decision terrains they have historically approached with caution or distance.” (KPMG) |

Numbers That Moved

| ▶ $3.7T of unsold PE assets globally; 16,000 companies held 4+ years (highest proportion on record). The inventory problem is now structural (Bain 2026) |

| ▶ GP-led secondaries value tripled from $35bn in 2020 to $115bn in 2025. Continuation vehicles are becoming a mainstream liquidity tool, not an emergency one (McKinsey 2026) |

| ▶ Operating groups doubled: centralised ops platforms have doubled in size since 2021, with 60% now used during DD. Operating alpha is becoming a fundraising prerequisite (McKinsey) |

AI News, Insights & Trends

| The future of AI is in court - The wave of AI copyright and licensing cases is becoming the defining backdrop for enterprise deployment. |

| Google bets $40bn on Anthropic - The latest leg of the frontier-lab capital cycle, and the deepening cloud-AI couplings. |

| A million jobs at risk in London - New labour-market modelling on AI displacement risk in financial services and professional services. |

| OpenAI launches GPT-5.5 - Step-change capability release. Worth re-running internal benchmarks across portco workflows. |

| SpaceX option to buy Cursor - Industrial buyers of AI vendors are now appearing alongside the PE buyers. |

Sources & References

| Google Cloud / Bloomberg - 22 April 2026 - Vista Equity x Google Cloud multiyear agentic AI deal across 90+ portfolio companies, including Gemini, AI Hypercomputer and Gemini Enterprise |

| KKR / Oak Hill Capital - 7 January 2026 - $1.5bn KKR + $400m Oak Hill commitment to Global Technical Realty European data centre platform |

| TechCrunch / Fortune - 26 March 2026 - Shield AI $1.5bn Series G at $12.7bn valuation, Advent + JPMorgan + $500m Blackstone preferred |

| a16z Enterprise AI Pulse 2026 - 72% of enterprises with AI in production (20% in 2020, 55% in 2024) |

| McKinsey Global Private Markets 2026 - Operating groups doubled since 2021, 60% in DD, $34bn top-100 alt M&A, GP-led secondaries $35bn (2020) to $115bn (2025) |

| KPMG Global M&A Outlook 2026 - 71% of PE firms pursuing carve-outs, 77% say activity rising, 73% AI in DD up from 24% |

| LCD / PitchBook - 91% of US leveraged loans are covenant-lite, default rate 5.7% early 2025 |

| Bain Global PE Report 2026 - $3.7T unsold PE assets, 16,000 companies held 4+ years |

| G3NR8 OEX deployment - PE-backed global technology and engineering firm: 4.5 FTEs of manual work eliminated, under 12 weeks to production |

Frequently Asked Questions

|

What is the Vista Equity Google Cloud agentic AI partnership? Announced on 22 April 2026, Vista Equity Partners signed a multiyear deal with Google Cloud to deploy agentic AI across its 90+ software portfolio companies. The package includes Gemini, the AI Hypercomputer super-computing system, and Gemini Enterprise for building portco-specific AI agents. Vista’s portfolio serves more than 2.5 million enterprise customers and 750 million users worldwide. |

|

How much did KKR invest in Global Technical Realty? On 7 January 2026, KKR committed an additional $1.5bn in equity to GTR, a European data centre platform. Oak Hill Capital joined with $400m, taking total commitments to nearly $2bn. The investment supports GTR’s development pipeline of greenfield data centre capacity for hyperscale, cloud and AI workloads. KKR is funding it primarily from its Global Infrastructure Strategy. |

|

What is Shield AI’s Series G deal? On 26 March 2026, Shield AI closed a $1.5bn Series G co-led by Advent International and JPMorgan Chase’s Security and Resiliency Initiative, with $500m of Blackstone preferred equity and a $250m delayed-draw facility, at a $12.7bn valuation. Advent chairman David Mussafer joins the board. The structure mirrors the OpenAI joint venture terms: PE preferred equity, board influence, and defined enterprise commitments. |

|

What does the enterprise AI saturation curve show? a16z data shows enterprise AI in production rose from 20% of enterprises in 2020 to 55% in 2024 to 72% in 2026. The S-curve steepened sharply through 2024 and is now at deployment saturation pace, not adoption. For PE, this means a portco with no AI in production is no longer a normal company on the curve, it is an outlier. |

|

What three things separate top-decile PE platforms from the rest? First, they run portfolios as a system, not a set of LP commitments: operating groups have doubled since 2021 and 60% of firms now deploy ops teams during DD. Second, they build their own operational early warning across the portfolio, replacing covenant-lite documentation with revenue-at-risk dashboards, order book intelligence, margin erosion signals and churn scoring. Third, they treat carve-outs as AI-native deployment environments because carve-outs arrive without legacy data infrastructure or parent-company IT governance. |

|

What is the OEX Marketing Intelligence deployment? G3NR8 deployed its OEX platform at a PE-backed global technology and engineering firm. The deployment combines a centralised knowledge base, AI search with natural-language querying, and an automated repurposing engine that turns source content into channel-ready, multi-language outputs in minutes. Results: 4.5 FTEs of manual work eliminated and under 12 weeks to production. The team is now compounding value with scheduled automation for case studies, Google Ads formats, expanded persona targeting and smarter search. |

|

PE Intelligence Platform - origination to exit. Screening, DD, 100-day, portfolio monitoring. Intelligence that compounds across deals. OEX for Portfolio Companies - operational efficiency deployed in 4 to 6 weeks. Revenue protection, knowledge capture, workflow automation. Working solutions, not pilots - small senior teams, model-agnostic, deployed and generating value from week one. |

This is Issue #6 of Operational Alpha - the bi-weekly AI briefing for PE operating partners. New issues publish every other week.

Keep informed with the newsletter for PE operating partners and the portfolio companies they back.

Get operational insights and trends, AI frameworks, resources and real deployment stories.