The whole industry just agreed on one thing

Jul 07, 2026Operational alpha for PE funds, their portfolio companies and operating partners. What we deliver: operational efficiency and speed to intelligence, AI that drives EBITDA, exits and DPI.

In this issue

- 📊 Deployment is the bottleneck, not better models

- 💸 The funds stopped pricing AI and started deploying it

- 🎯 The proof: EUR 45m of at-risk revenue found in 6 weeks

- 🔢 Numbers that moved

- 💡 Why G3NR8: the version a fund can actually buy

- 📰 On the radar

Make it yours

Two ways to shape it. Name a topic and we fold it into the next issue. Or get your own edition, on your themes, sent only to you, one-off or fortnightly.

Tell us what you wantThe industry just agreed the bottleneck is deployment, not models.

In the space of a fortnight, the three biggest AI platforms staked more than a billion dollars each on one idea: getting from a pilot to a working system is a people-on-the-ground problem. They are right. They just are not sending those people to the mid-market.

The read: the platforms have concluded the gap is deployment, not licences, and they are buying their way across it.

On 30 June, AWS committed one billion US dollars to a forward-deployed-engineer unit, pods of five to six people placed inside enterprise customers to move AI from pilot to production. It follows OpenAI's ten-billion-dollar Deployment Company and Anthropic's 1.5-billion-dollar joint venture, both announced in May. Three vendors, three enormous bets, one thesis: the model was never the hard part.

- AWS, one billion US dollars, pods of five to six embedded inside named launch customers (CNBC).

- The confirmed line from the AWS lead: the currency customers keep asking for is speed.

- The uncomfortable part for a mid-market portfolio: those pods chase the largest, most data-rich accounts, where the compute revenue is.

Source: CNBC, 30 June 2026

Every quarter a portfolio company's AI sits stuck in pilot is EBITDA left on the table, and an unanswered diligence question at exit. The build-versus-buy answer is now settled in principle: you need someone who embeds. The only open question is who does that at the scale of a mid-market operating company, and turns a stalled pilot into protected EBITDA before the next investment committee. Protected value, a more defensible multiple, distributions to paid-in capital (DPI), the next raise.

The read: the winning question moved from "what is AI worth to this asset" to "how fast can this asset put AI to work".

Three of the largest funds answered the same question three ways in a fortnight. Tech buyout value froze, because buyers could not price software against an uncertain AI future. Thoma Bravo called the scare over, its evidence its own book. And KKR ignored the pricing debate entirely, buying a labour-heavy accounting firm precisely because AI is about to rewrite the work inside it.

- Technology buyout value fell roughly 70% in the first quarter, to about $20bn, as buyers could not price software against an uncertain AI future (Bain / Dealogic, via Bloomberg).

- Thoma Bravo, running nearly $200bn, says about 50% of new revenue across its portfolio now comes from AI and agentic products (SuperReturn International; CNBC).

- KKR took a majority of Crowe, a $1.39bn-revenue accounting firm with more than 9,000 staff, at nearly $3bn: a bet on how fast AI rewrites the work inside a people business (Wall Street Journal, June 2026).

Source: Bain / Dealogic via Bloomberg; SuperReturn International / CNBC; Wall Street Journal, June 2026.

Speed of deployment is the one game a mid-market fund can win. It will not out-bid a $3bn take-private or run a $200bn platform, but it can move faster inside the portfolio companies it already owns, and turn that speed into earnings before the next investment committee.

- › 7% of private-equity-backed companies run AI at enterprise scale; the leading tier posts 18% more AI-related exits on the same spend, from operating-model design, not a bigger cheque (FTI Consulting 2026 PE AI Radar, 19 May 2026).

- › $1tn+ global data-centre capex is forecast for 2026, the first year the number carries a trillion, after the four largest US cloud providers raised first-quarter spend 78% year on year (Dell'Oro Group, 10 June 2026).

- › +8% vs flat US dealmaking above $100m grows 8% in 2026 while private equity stays flat, and 65% of CEOs pursuing M&A say they are buying technology, talent and operating capability (EY-Parthenon, 2 June 2026).

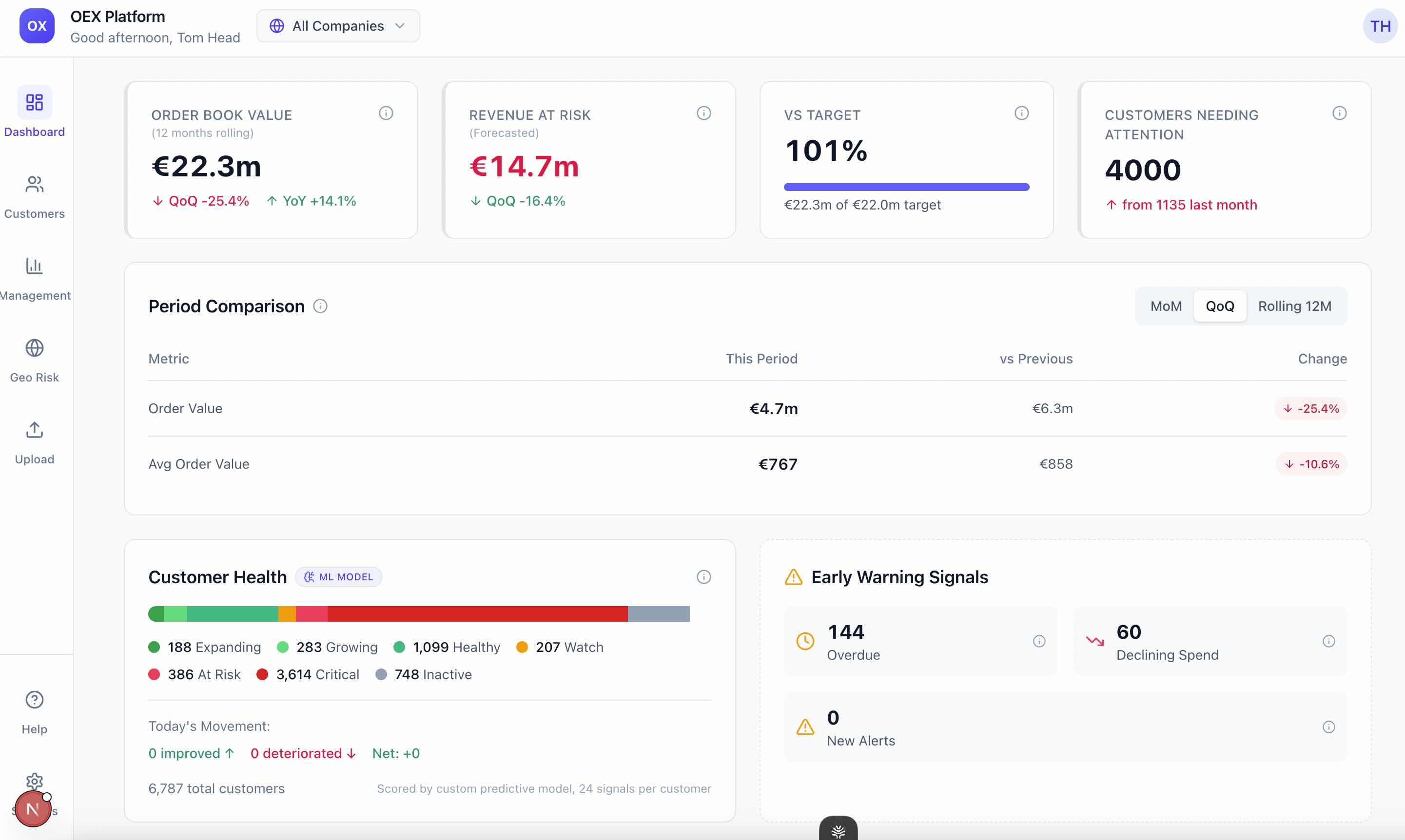

a European industrial distributor

The signals above describe a fix the mega-scale players are buying for themselves. Here is what the mid-market version looks like when it works. We connected to a distributor's order data, as it was, and surfaced revenue their sales team could not see. Intelligence and automation, in weeks, not an eighteen-month programme. This is OEX, our Operational Excellence platform, and it runs on the same cost curve the labs are driving down.

That is not a slide. It is production, and the at-risk revenue OEX protects is the revenue that underwrites the exit multiple. A documented, defensible operational-alpha story is exactly what a LP wants to see before committing to the next fund: protected revenue, a de-risked and higher-multiple asset, DPI, the next raise.

The version a fund can actually buy

The operational drag inside almost every portfolio company looks the same:

- › Fragmented data spread across systems that do not talk to each other

- › Slow intelligence, where a straight question takes days to answer

- › Repetitive manual work soaking up the commercial team's time

- › Invisible churn, customers drifting away before anyone sees it

- › Risk and margin leakage that only surface once they hit the P&L

We turn that operational drag into working intelligence and automation, at the asset, in weeks.

- › Revelstoke Capital launched a permanent in-house AI function, the build route to what a fractional capability delivers without the fixed overhead.

- › S&P Global found 72% of general partners now name operations the top value lever, yet 75% say their AI tools are ineffective at portfolio monitoring. Intent without instrumentation.

- › Bain reports distributions matching crisis-era lows for a fourth straight year, the duration now a record. The fundraising squeeze in one number.

- › Middle Market Growth argues operating partners get accountability without authority: put AI where it lowers cost or lifts conversion, not where it photographs well on a slide.

See where the revenue is leaking, and where it is growing.

Ask us for the free data read and we will scope a rapid read of one portfolio company's own data: where revenue is at risk, where the growth is, and how its customers benchmark against each other. The same analysis we ran for a European industrial distributor, under a mutual NDA.

Ask us for the free data readThe mega-scale players are proving the category and buying the fix for themselves. The version a mid-market fund can actually buy is operational alpha, delivered at the asset by a small team that embeds for weeks. That is the whole ladder, and every rung is one we already stand on.

Tom

P.S. Tell us what you want more of, the market read or the deployment detail.

Keep informed with the newsletter for PE operating partners and the portfolio companies they back.

Get operational insights and trends, AI frameworks, resources and real deployment stories.